Every thriving business runs on numbers — and behind those numbers are two distinct disciplines that are often confused, conflated, or used interchangeably. Bookkeeping and accounting are not the same thing. Both are essential. Both protect your bottom line. But they serve fundamentally different purposes, operate at different levels of complexity, and require different skills. Understanding the distinction is not just an academic exercise — it directly impacts how you structure your financial team and whether outsourced bookkeeping could be the competitive advantage your business has been missing.

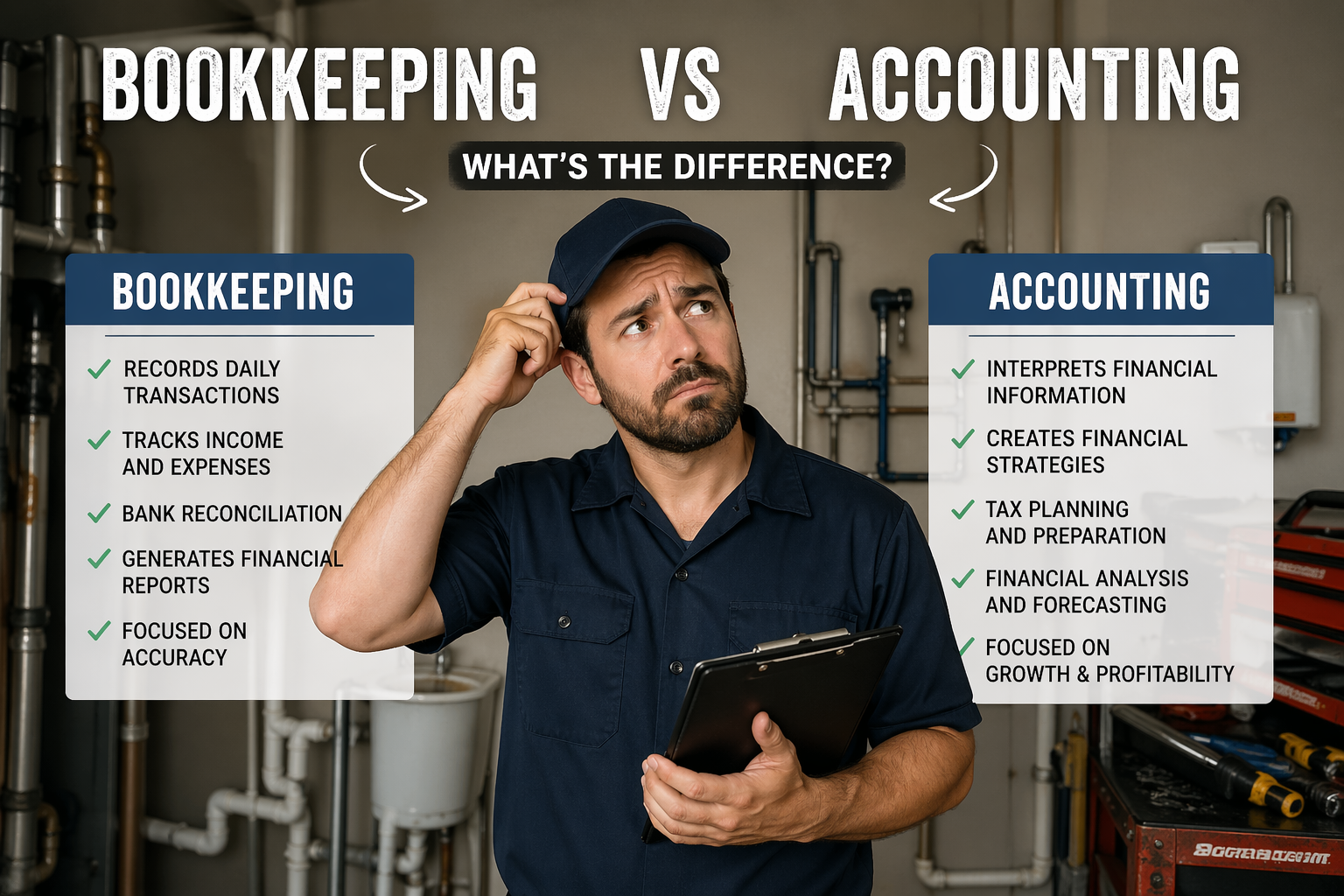

What Is Bookkeeping?

Bookkeeping is the systematic recording, organizing, and storing of financial transactions. It is the foundational layer of your business finances — the daily discipline of capturing every dollar that flows in and out. Think of bookkeeping as the raw data collection phase of your financial operation.

A bookkeeper's core responsibilities include recording sales, purchases, receipts, and payments; reconciling bank and credit card statements; managing accounts payable and accounts receivable; processing payroll; and maintaining the general ledger. These tasks are transactional, detail-oriented, and require accuracy above all else.

"Bookkeeping is the financial backbone of your business — without clean books, every other financial decision is built on sand."

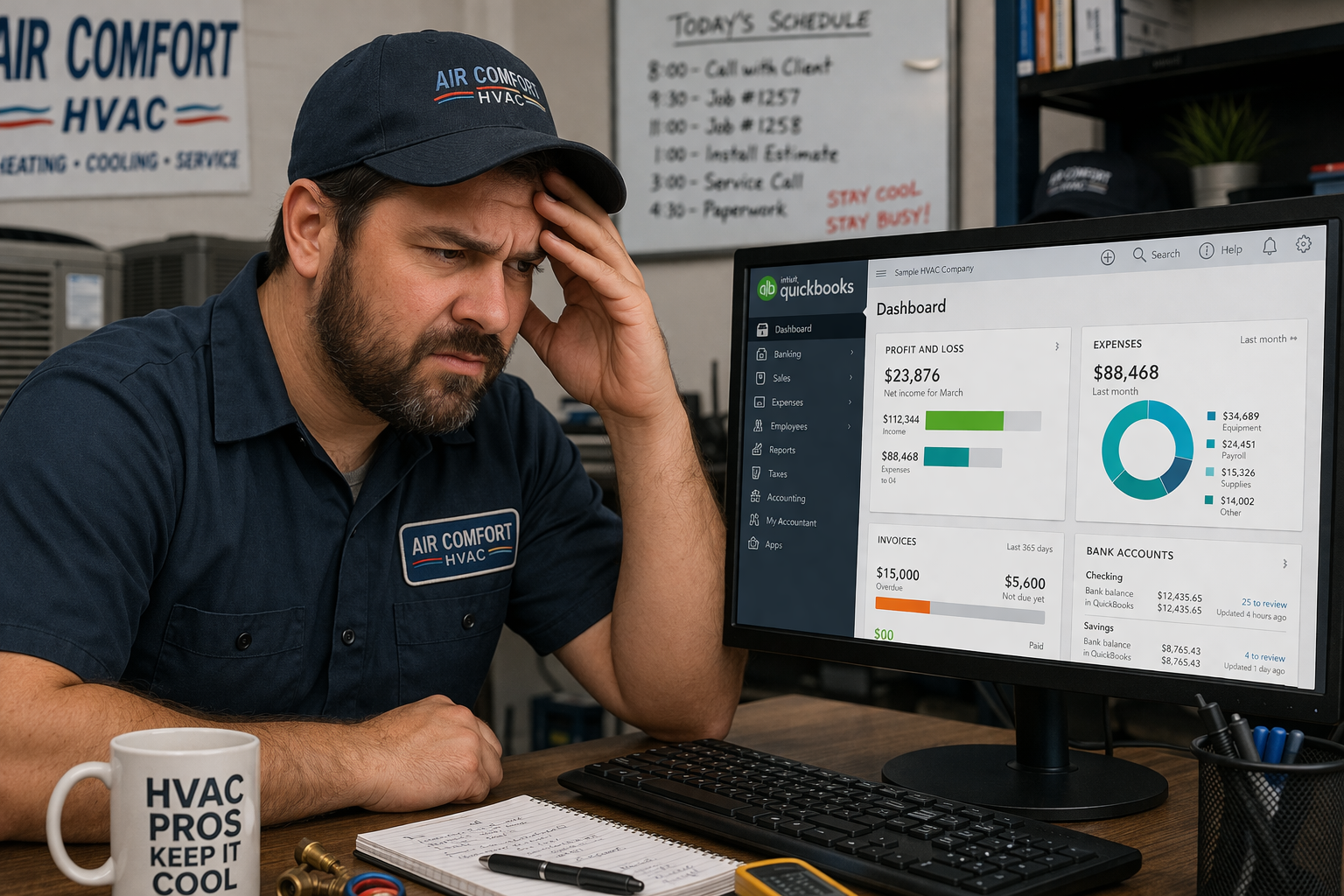

Bookkeeping does not require a CPA license. A skilled bookkeeper uses tools like QuickBooks, Xero, or FreshBooks to maintain clean, organized records that paint an accurate picture of where your money has been. The emphasis is on precision, consistency, and timeliness. When your books are current and accurate, everything downstream — tax filing, financial reporting, strategic planning — becomes dramatically easier.

What Is Accounting?

Accounting takes the data produced by bookkeeping and transforms it into insight. While bookkeeping records what happened, accounting interprets what it means — and what you should do about it.

Accountants analyze financial statements, identify trends, assess profitability, manage tax strategy, ensure regulatory compliance, and provide the financial intelligence business owners need to make informed decisions. They prepare income statements, balance sheets, and cash flow statements. They advise on entity structure, depreciation, deductions, and long-term financial planning.

Most accountants — particularly CPAs — have earned advanced degrees and professional certifications. They are strategic advisors as much as they are financial professionals. Where a bookkeeper ensures your records are accurate, an accountant ensures those records are being used to drive your business forward.

Bookkeeping vs Accounting: Side-by-Side

| Factor |

Bookkeeping |

Accounting |

| Primary Function |

Record & organize transactions |

Analyze & interpret financial data |

| Focus |

Day-to-day accuracy |

Strategic insight & compliance |

| Output |

Ledgers, reconciliations, reports |

Financial statements, tax filings, forecasts |

| Credentials Required |

No license required |

CPA or equivalent often needed |

| Decision-Making Role |

Operational |

Strategic |

| Frequency |

Daily / weekly |

Monthly, quarterly, annually |

| Cost |

Lower |

Higher |

Why Both Matter — And Why They Work Together

Neither bookkeeping nor accounting can fully replace the other. They are complementary disciplines that form a complete financial ecosystem for your business. Accounting is only as good as the books it draws from — garbage in, garbage out. If your bookkeeping is disorganized, inconsistent, or months behind, your accountant cannot provide the strategic guidance you need. They will spend billable hours cleaning up records instead of delivering value.

Conversely, meticulous bookkeeping without proper accounting leaves your business flying blind on the strategic level. You may know how much came in last Tuesday, but you won't know whether your business model is truly profitable, what your effective tax rate should be, or how to structure a loan for expansion.

Key Distinctions at a Glance

- Bookkeeping is about recording; accounting is about understanding

- Clean books make tax season far less stressful and costly

- Accountants rely on bookkeepers for accurate source data

- Both functions are essential at every stage of business growth

- Outsourcing bookkeeping often delivers better accuracy than in-house

- The right financial team protects you from costly compliance errors

The Case for Outsourced Bookkeeping

Here is where many small and mid-sized business owners find their greatest opportunity: outsourced bookkeeping. Rather than hiring a full-time, in-house bookkeeper — with all the associated costs of salary, benefits, training, and management overhead — businesses increasingly turn to professional outsourced bookkeeping providers to handle this critical function at a fraction of the cost.

Outsourced bookkeeping means engaging a dedicated team or firm to manage your day-to-day financial recordkeeping remotely. The books are maintained with the same rigor and accuracy as if you had an in-house professional, but the structure is more flexible, more cost-effective, and often more reliable.

The Real Benefits of Outsourced Bookkeeping

Cost efficiency. A full-time bookkeeper can cost $45,000–$65,000 per year in salary alone, before benefits. Outsourced bookkeeping typically costs a fraction of that, with no HR overhead, no benefits administration, and no downtime when your employee takes a vacation or falls ill.

Access to expertise. Outsourced bookkeeping firms employ professionals who specialize in bookkeeping — this is all they do, all day. That specialization translates to faster, more accurate work, and deeper familiarity with the nuances of your accounting software. You get seasoned professionals, not someone who is learning on the job with your financials.

Scalability. Your business grows. Your bookkeeping needs change. An outsourced model scales with you — seamlessly, without the friction of hiring, training, or restructuring a team.

Cleaner books, better accounting. When your outsourced bookkeeping is done right, your accountant has exactly what they need to do their best work. This creates a virtuous cycle: clean data enables sharp analysis, which enables smarter decisions, which drives growth.

Reduced risk. Errors in financial recordkeeping can lead to penalties, tax issues, and cash flow crises. Professional outsourced bookkeeping reduces the risk of human error and ensures your records are always audit-ready.

When Should You Start Outsourcing Your Bookkeeping?

The honest answer is: sooner than you think. Many business owners wait until they are overwhelmed — books months behind, tax deadlines looming, cash flow unclear — before they seek help. That reactive approach is expensive and stressful. The proactive approach is to build a solid financial foundation from early on, so that every growth milestone is supported by accurate, timely financial data.

Whether you are a solopreneur growing into your first hire, a small business with $500K in revenue, or a mid-sized operation with multiple departments, outsourced bookkeeping can deliver immediate, tangible value. The investment is modest. The return — in time, clarity, and peace of mind — is substantial.

"The question isn't whether you can afford outsourced bookkeeping — it's whether you can afford the cost of disorganized books."

Making the Right Choice for Your Business

Understanding bookkeeping vs accounting is the first step. The second step is ensuring your business has the right structure in place. For most growing businesses, the answer is a combination: outsourced bookkeeping to maintain clean, accurate records day-to-day, paired with a skilled accountant to provide strategic financial guidance on a periodic basis.

At AcctSage, we specialize in helping business owners get clarity on their finances — starting with professional outsourced bookkeeping that gives you and your accountant the foundation you need. Clean books. Actionable insights. Financial peace of mind. That is what we deliver.

Free Discovery Call

Ready to Clean Up Your Books?

Let's talk about your business finances. Book a free consultation with our team and discover how outsourced bookkeeping can save you time, reduce risk, and drive smarter decisions.

Schedule Your Free Call →

No obligation · 30-minute session · Tailored to your business

-1.png)